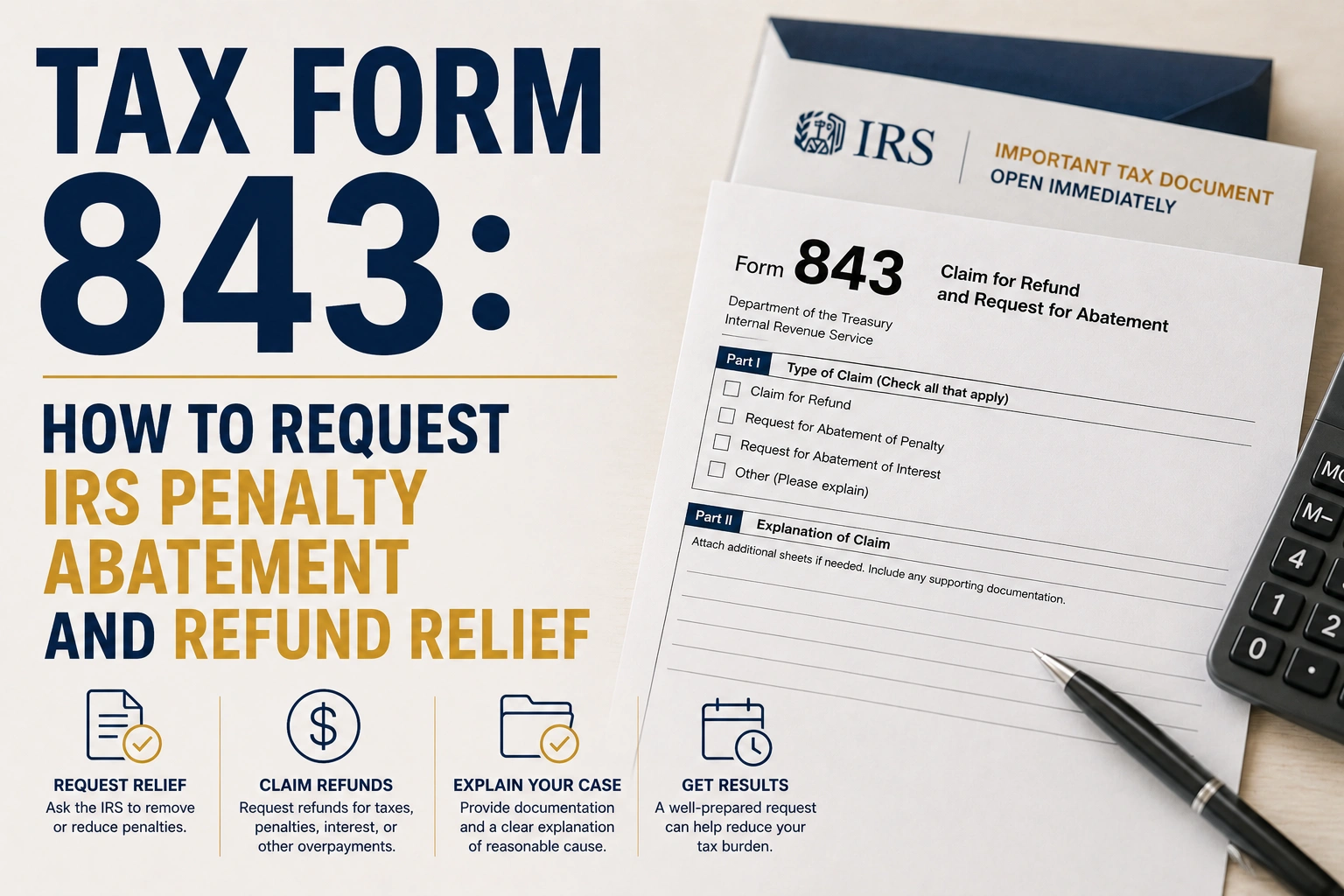

If you owe IRS penalties or believe you paid taxes incorrectly, understanding how to use IRS tax form 843 may help you request financial relief directly from the Internal Revenue Service.

Many taxpayers searching for answers about request for abatement options, first-time penalty forgiveness, or IRS refund claims eventually discover Form 843 Claim for Refund and Request for Abatement. However, incorrectly completing the form, mailing it to the wrong location, or misunderstanding eligibility rules can delay relief or lead to rejection.

At Tax Law Advocates, tax attorney Yongho David Cho and enrolled agent Jamie Roman frequently help taxpayers navigate IRS penalty disputes, refund claims, and abatement requests involving late filing penalties, failure-to-pay penalties, payroll tax issues, and reasonable cause relief.

This guide explains:

- What is Form 843

- Who qualifies for penalty abatement

- How to fill out Form 843 for first time abatement

- Where to file Form 843

- Form 843 mailing address rules

- Common mistakes that trigger denials

- When taxpayers should seek professional legal guidance

What Is Form 843?

IRS Form 843 is officially called:

Form 843 — Claim for Refund and Request for Abatement

The form allows taxpayers to request:

- Removal of IRS penalties

- Interest abatement in limited cases

- Certain tax refunds

- Corrections involving employment taxes

- Refunds of penalties paid in error

Many taxpayers refer to it online as:

- tax abatement form

- penalty abatement form

- fabatement form

- abatement form 843

- request for abatement form

The most common use of tax form 843 is requesting IRS penalty abatement.

What Can Form 843 Be Used For?

Penalty Abatement Requests

This is the most common use of form 843 penalty abatement requests.

Taxpayers may request removal of:

First-Time Penalty Abatement

Some IRS penalties are more likely to qualify for relief than others. Failure to File penalties are often the most commonly approved for penalty abatement, especially under First-Time Abatement rules. Failure to Pay penalties may also qualify in certain cases. Estimated Tax Penalties usually have limited eligibility, while Payroll Tax Penalties often require a detailed case review. Accuracy-related penalties generally require strong supporting evidence and documentation before the IRS considers relief.

Form 843 first time abatement

The IRS may remove penalties if the taxpayer:

- Has a clean compliance history

- Filed required returns

- Is currently compliant

- Did not previously receive FTA recently

Many people searching “how to fill out form 843 for first time abatement” are trying to qualify under this IRS administrative waiver program.

Claim for Refund Requests

The form may also be used for:

- Refunds of penalties already paid

- Certain employment tax corrections

- Improper IRS assessments

- Interest adjustments in limited cases

This is why the official title includes:

form 843 claim for refund and request for abatement

Who Qualifies for IRS Penalty Abatement?

IRS relief is not automatic.

The IRS generally reviews:

- Compliance history

- Filing history

- Payment history

- Cause of the issue

- Supporting documentation

- Whether circumstances were outside the taxpayer’s control

Common Reasonable Cause Examples

Potential reasonable cause situations include:

- Serious illness

- Death in the family

- Natural disasters

- Records destroyed by fire or theft

- Reliance on incorrect professional advice

- IRS processing errors

Attorney Yongho David Cho notes that many taxpayers mistakenly assume hardship alone guarantees approval. In reality, the IRS evaluates documentation, timelines, and compliance behavior carefully.

Form 843 Instructions: Step-by-Step Guide

Many taxpayers searching for form 843 instructions or how to file form 843 are unsure how detailed their explanation should be.

Below is a simplified overview.

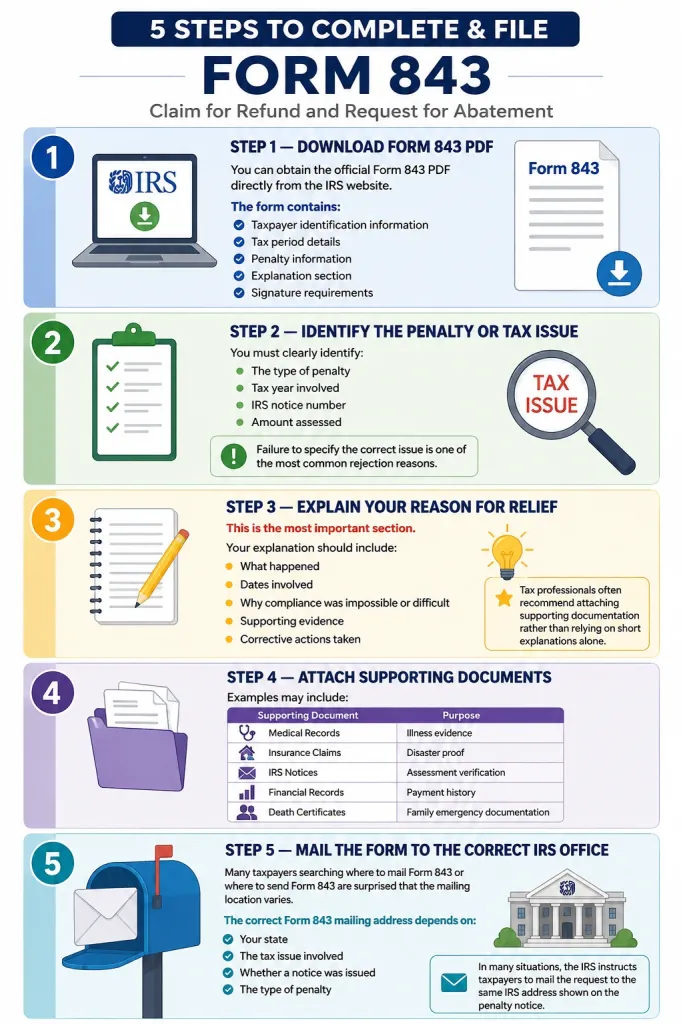

Step 1 — Download Form 843 PDF

You can obtain the official form 843 pdf directly from the IRS website.

The form contains:

- Taxpayer identification information

- Tax period details

- Penalty information

- Explanation section

- Signature requirements

Step 2 — Identify the Penalty or Tax Issue

You must clearly identify:

- The type of penalty

- Tax year involved

- IRS notice number

- Amount assessed

Failure to specify the correct issue is one of the most common rejection reasons.

Step 3 — Explain Your Reason for Relief

This is the most important section.

Your explanation should include:

- What happened

- Dates involved

- Why compliance was impossible or difficult

- Supporting evidence

- Corrective actions taken

Tax professionals often recommend attaching supporting documentation rather than relying on short explanations alone.

Step 4 — Attach Supporting Documents

Examples may include:

When submitting Form 843, attaching strong supporting documentation can significantly improve the chances of approval. Common documents include medical records to prove illness, insurance claims as evidence of natural disasters or unexpected events, IRS notices to verify the assessment in question, and financial records to demonstrate payment history or financial circumstances. In cases involving family emergencies, taxpayers may also include death certificates or related documentation to support their reasonable cause explanation.

Step 5 — Mail the Form to the Correct IRS Office

Many taxpayers searching where to mail form 843 or where to send form 843 are surprised that the mailing location varies.

The correct form 843 mailing address depends on:

- Your state

- The tax issue involved

- Whether a notice was issued

- The type of penalty

In many situations, the IRS instructs taxpayers to mail the request to the same IRS address shown on the penalty notice.

Where to File Form 843

The answer to where to file form 843 depends on your case.

Common mailing destinations include:

- IRS service centers

- Addresses listed on IRS notices

- Specialized IRS processing units

Because mailing rules can change, taxpayers should verify the latest address instructions directly with the IRS before submission.

Can You Efile Form 843?

Many taxpayers search for efile form 843 options.

Currently, the IRS generally requires Form 843 to be submitted by mail for most penalty abatement requests.

Electronic filing options remain limited compared to standard income tax returns.

Form 843 Example: What a Successful Request Looks Like

Example Scenario

A taxpayer filed late after being hospitalized unexpectedly for several months.

The taxpayer:

- Had a clean filing history

- Filed immediately after recovery

- Paid taxes owed

- Included hospital documentation

- Submitted a detailed explanation

The IRS may approve removal of the failure-to-file penalty under reasonable cause standards.

This type of form 843 sample situation is often stronger when the taxpayer demonstrates both compliance history and documented hardship.

Common Mistakes That Lead to Form 843 Denials

Incomplete Explanations

The IRS rarely approves vague statements.

Missing Documentation

Lack of supporting records significantly weakens requests.

Filing Before Becoming Compliant

Taxpayers generally must file required returns before requesting relief.

Sending the Form to the Wrong Address

Incorrect mailing locations can delay processing for months.

Requesting Relief for Ineligible Penalties

Not every IRS penalty qualifies for removal.

How Long Does Form 843 Take?

IRS processing times for Form 843 can vary widely depending on several factors. An existing IRS backlog may cause longer delays, while more complex cases often require additional review by the agency. Requests submitted with missing documents or incomplete explanations may face rejection or significant processing delays. Cases involving payroll tax penalties typically receive closer scrutiny and can take even longer to resolve.

Some requests may take several months before a final determination is issued.

When Should You Contact a Tax Attorney?

Complex situations often require professional review, especially involving:

- Large IRS balances

- Business payroll tax penalties

- Multiple years of noncompliance

- Appeals disputes

- Collection enforcement

- IRS liens or levies

At Tax Law Advocates, Yongho David Cho and Jamie Roman assist taxpayers nationwide with IRS penalty disputes, reasonable cause analysis, first-time abatement requests, and broader tax resolution strategies.

Frequently Asked Questions About Tax Form 843

What is Form 843 used for?

Form 843 is used to request penalty abatement, certain tax refunds, interest relief, or correction of IRS assessments.

Can I use Form 843 for first-time penalty abatement?

Yes. Many taxpayers use Form 843 to request First-Time Abatement (FTA) for failure-to-file or failure-to-pay penalties.

Can Form 843 be filed electronically?

In most cases, no. Most Form 843 requests must currently be mailed to the IRS.

Where do I mail Form 843?

The correct mailing address depends on the type of penalty and your IRS notice. Many taxpayers should mail the form to the address listed on their IRS correspondence.

How long does the IRS take to process Form 843?

Processing times vary and may take several weeks or months depending on complexity and IRS backlog conditions.

Does filing Form 843 stop IRS collections?

Not automatically. The IRS may continue collection activity while reviewing the request unless additional arrangements are made.

Can interest also be removed?

In limited situations, yes. However, interest relief rules are stricter than penalty abatement rules.

Final Thoughts on IRS Tax Form 843

Understanding how to properly complete and submit tax form 843 can make a major difference when requesting IRS penalty relief or refunds.

A well-prepared request supported by documentation, compliance history, and accurate legal reasoning is far more likely to succeed than a generic explanation.

For taxpayers facing serious IRS penalties, aggressive collection activity, or complex compliance problems, experienced representation may help reduce financial exposure and improve negotiation outcomes.

Tax Law Advocates provides nationwide assistance for IRS penalty abatement, first-time abatement requests, tax resolution matters, and complex IRS disputes.