When taxpayers fall behind on IRS debt and fail to respond to collection notices, the government may escalate enforcement actions through a tax levy. Many people confuse a tax levy with a tax lien, but they are very different legal actions with serious financial consequences.

A levy allows the IRS or state tax authority to legally seize assets, freeze bank accounts, garnish wages, or take property to satisfy unpaid taxes. Understanding how a levy works is critical because once enforcement begins, access to money and property can become severely restricted.

At Tax Law Advocates, tax professionals including Yongho David Cho and Jamie Roman help taxpayers analyze IRS levy notices, negotiate collection alternatives, and pursue levy release strategies before assets are permanently seized.

What Is a Tax Levy?

A tax levy is a legal collection action that allows the IRS or state tax agency to take assets directly from a taxpayer to satisfy unpaid tax debt.

Tax Levy Definition

The tax levy definition refers to the government’s legal authority to seize:

- Bank accounts

- Wages

- Social Security benefits

- Business income

- Real estate

- Vehicles

- Investment accounts

- Rental income

In simple terms, a levy means the government is no longer merely requesting payment — it is actively collecting through forced seizure.

Many taxpayers search:

- What is a tax levy

- What levy means

- Define levy taxes

- Levy taxes def

- What does levy taxes mean

All generally refer to the same concept: enforced collection of unpaid taxes.

How Does a Levy Work?

The IRS cannot usually levy assets without first following a legal process.

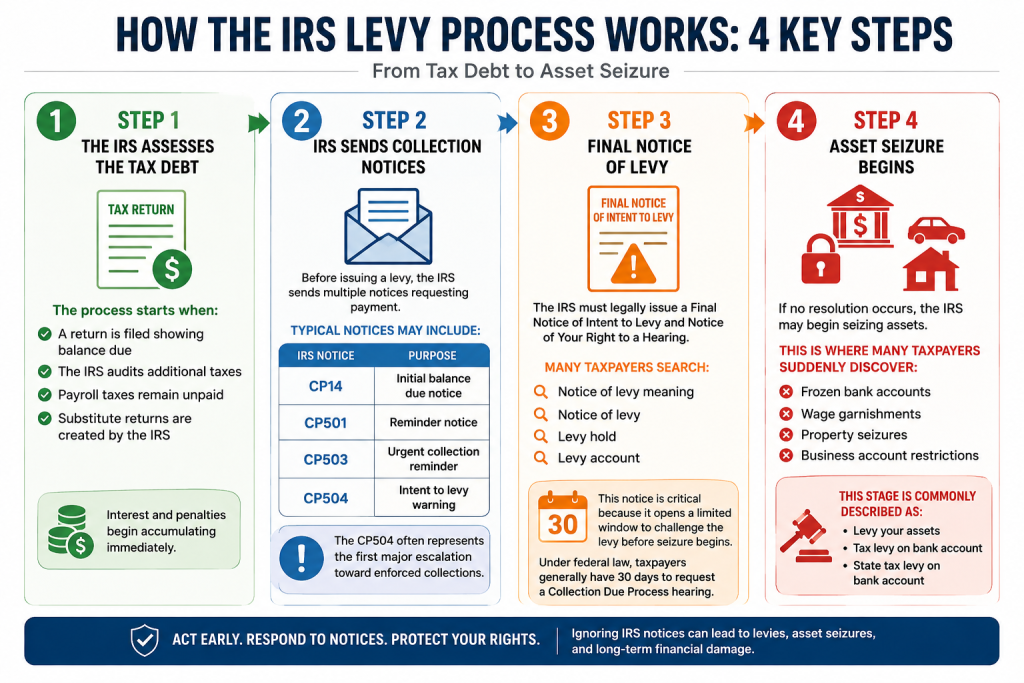

Step 1 — The IRS Assesses the Tax Debt

The process starts when:

- A return is filed showing balance due

- The IRS audits additional taxes

- Payroll taxes remain unpaid

- Substitute returns are created by the IRS

Interest and penalties begin accumulating immediately.

Step 2 — IRS Sends Collection Notices

Before issuing a levy, the IRS sends multiple notices requesting payment.

Before issuing a tax levy, the IRS typically sends several collection notices warning taxpayers about unpaid balances and escalating enforcement actions. The process usually begins with a CP14 notice, which informs the taxpayer of an initial balance due. If the debt remains unresolved, the IRS may then issue a CP501 reminder notice followed by a CP503 urgent collection reminder.

One of the most serious warnings is the CP504 notice, which signals the IRS’s intent to levy and represents a major escalation toward enforced collection actions such as bank levies or wage garnishments.

Step 3 — Final Notice of Levy

The IRS must legally issue a Final Notice of Intent to Levy and Notice of Your Right to a Hearing.

Many taxpayers search:

- Notice of levy meaning

- Notice of levy

- Levy hold

- Levy account

This notice is critical because it opens a limited window to challenge the levy before seizure begins.

Under federal law, taxpayers generally have 30 days to request a Collection Due Process hearing.

Step 4 — Asset Seizure Begins

If no resolution occurs, the IRS may begin seizing assets.

This is where many taxpayers suddenly discover:

- Frozen bank accounts

- Wage garnishments

- Property seizures

- Business account restrictions

This stage is commonly described as:

- Levy your assets

- Tax levy on bank account

- State tax levy on bank account

How Does a Tax Levy Work on a Bank Account?

A bank levy is one of the most aggressive IRS collection tools.

IRS Bank Levy Process

Once the levy is served:

- The bank freezes available funds

- The account enters a holding period

- The taxpayer temporarily loses access

- Funds may be transferred to the IRS after the hold expires

Many taxpayers search:

- Levy account

- Levy hold

- Levy charges

- State tax levy on bank account

The holding period usually lasts 21 days for federal IRS levies, creating a short opportunity to negotiate a release.

What Happens During a Levy Hold?

A levy hold means the bank freezes money currently available in the account.

During this period:

- Debit cards may stop working

- Automatic payments may fail

- Payroll deposits may become inaccessible

- Mortgage or rent payments may bounce

For business owners, payroll disruption can create major operational risks.

What Is a Levy on Property?

A levy can also apply to physical assets.

What Is a Tax Levy on Property?

A property levy may involve:

- Real estate

- Vehicles

- Boats

- Business equipment

- Rental properties

Many people search:

- What is a levy on property

- What is a tax levy on property

- Current tax levy meaning on property

This refers to the government’s ability to legally seize and potentially sell property to satisfy tax debt.

Tax Levy vs Tax Lien

Many taxpayers confuse liens and levies.

Current Tax Levy Meaning Explained

The phrase current tax levy meaning usually refers to an active collection action already in progress.

This may indicate:

- Active wage garnishment

- Frozen bank accounts

- IRS seizure authority

- State tax collection enforcement

Taxpayers often discover a current levy only after:

- A direct deposit disappears

- A paycheck shrinks

- A bank account freezes

- A title issue appears during refinancing

What Is a Levy in Law?

Legal Meaning of Levy

In legal terms, a levy refers to the authorized seizure of property to satisfy a debt or legal obligation.

Outside tax law, levies may occur in:

- Civil judgments

- Child support enforcement

- Court debt collections

- State agency recoveries

However, IRS tax levies carry unique federal collection powers that can move very quickly.

What Is a Tax Levy Fee?

Some taxpayers notice additional costs associated with collection actions.

Levy Charges and Collection Costs

A tax levy can trigger several additional costs beyond the original tax debt. These may include bank processing fees charged by financial institutions, ongoing interest accrual while the levy remains in effect, failure-to-pay penalties assessed by the IRS, and legal or professional representation expenses incurred while resolving the matter. Over time, these added costs can significantly increase the total amount owed if the levy is not addressed promptly.

Possible levy-related expenses may include:These additional costs can significantly increase total tax debt over time.

Can the IRS Levy Your Assets Without Warning?

Usually, no.

Federal law generally requires:

- Notice of tax assessment

- Demand for payment

- Final notice of intent to levy

- Opportunity for appeal

However, ignoring notices may cause taxpayers to miss critical deadlines.

At Tax Law Advocates, Yongho David Cho often explains that many levy cases become more difficult simply because taxpayers delay responding until bank accounts are already frozen.

How to Stop a Tax Levy

Several legal strategies may stop or release a levy depending on the taxpayer’s financial condition.

Common Tax Levy Relief Options

Several IRS resolution options may help stop or reduce collection activity. An Installment Agreement allows taxpayers to make structured monthly payments, while an Offer in Compromise may settle qualifying tax debt for less than the full amount owed. Currently Not Collectible status can temporarily suspend collection efforts for those facing financial hardship. Other options include Penalty Abatement to reduce qualifying penalties, Collection Appeals to challenge levy actions, and bankruptcy analysis to determine whether certain tax debts may be eligible for discharge under federal law.

Tax professionals like Jamie Roman help taxpayers evaluate which collection alternatives may qualify based on income, assets, hardship status, and IRS compliance history.

Why Early Action Matters in Levy Cases

The earlier taxpayers respond, the more options usually remain available.

Waiting too long can result in:

- Empty bank accounts

- Wage garnishments

- Business shutdown risks

- Property seizures

- Escalating penalties

- Long-term financial damage

In many cases, early intervention allows attorneys to negotiate before actual seizure occurs.

When Should You Contact a Tax Attorney About a Levy?

You should seek professional guidance immediately if you receive:

- Final Notice of Intent to Levy

- Bank levy notice

- Wage garnishment notice

- Property seizure warning

- IRS collection summons

- State tax levy notice

Tax levies involve strict deadlines and complex procedural rules that may affect appeal rights.

FAQs About Tax Levies

What is a tax levy?

A tax levy is a legal action allowing the IRS or state agency to seize assets to collect unpaid taxes.

How does a tax levy work?

The IRS assesses taxes, sends collection notices, issues a final warning, and may then seize assets such as bank accounts or wages.

What does levy mean on a bank account?

It means the account has been frozen or seized due to unpaid debt, often by the IRS or state tax authority.

What is a notice of levy?

A notice of levy is an official legal document informing taxpayers or financial institutions that the government intends to seize assets.

What is a levy on property?

A property levy allows the IRS to seize and potentially sell real estate or physical assets to satisfy unpaid taxes.

Can a tax levy be removed?

Yes. Depending on the case, levies may be released through payment arrangements, hardship status, appeals, or negotiated settlements.

Is a levy different from a tax lien?

Yes. A lien is a legal claim against property, while a levy is the actual seizure of money or assets.

What should I do after receiving a levy notice?

You should act immediately. Delays can reduce available legal options and increase the risk of asset seizure.

This article is for educational purposes only and does not constitute legal or tax advice. Viewing this page does not create an attorney-client relationship. IRS outcomes depend on your specific financial situation, documentation, compliance status, and procedural posture. If you have received time-sensitive IRS notices, seek qualified professional advice promptly.