Are debt relief programs legit? This is one of the most searched financial questions online today as millions of Americans struggle with rising credit card balances, collection accounts, medical debt, and personal loans. With inflation, high interest rates, and economic pressure affecting households nationwide, many consumers begin searching for solutions that promise lower payments, reduced balances, or complete financial recovery.

The reality is that some debt relief companies are legitimate, while others use aggressive marketing, misleading guarantees, or unrealistic promises to attract financially vulnerable consumers. Understanding the difference between a trustworthy debt relief strategy and a potentially harmful financial decision is critical because debt settlement directly affects credit scores, tax obligations, future borrowing ability, and even legal exposure.

Consumers searching online for answers like are debt relief programs worth it, how do debt relief programs work, or is debt relief a good idea are often already under financial pressure. That is why it is important to review debt relief programs carefully before enrolling in any service that claims to reduce or eliminate debt.

What Is a Debt Relief Program?

A debt relief program is a financial solution designed to help consumers reduce, restructure, negotiate, or manage outstanding debts. These programs are commonly used for unsecured debts such as credit cards, medical bills, collection accounts, and personal loans.

Types of Debt Commonly Included in Debt Relief

Most debt relief programs focus on unsecured debts because creditors may be more willing to negotiate balances that are not tied to collateral. Credit card debt is the most common type included, followed by medical bills, personal loans, and collection accounts. Some programs may also assist with tax debt, although IRS obligations often require specialized tax resolution strategies.

Debt Relief Is Not the Same as Debt Elimination

Consumers often misunderstand debt relief advertisements and assume balances simply disappear. In reality, most debt relief programs involve negotiations, structured settlements, or revised payment strategies. Even when debts are partially forgiven, there may still be credit consequences and potential tax obligations.

How Do Debt Relief Programs Work?

Understanding how do debt relief programs work is essential before agreeing to any contract or payment arrangement.

Most debt settlement programs follow a similar structure. First, the company reviews the consumer’s financial situation, including total debt balances, income, expenses, and delinquency status. After enrollment, the consumer usually stops making direct payments to creditors and instead deposits monthly funds into a dedicated account managed by the settlement company or a third-party processor.

The Negotiation Process

As the dedicated account balance grows, negotiators attempt to settle debts with creditors for reduced lump-sum payments. Creditors sometimes agree to accept less than the full balance if they believe repayment in full is unlikely.

This process can take several months or even years depending on the amount of debt involved.

Why Creditors May Agree to Settlements

Creditors sometimes prefer partial repayment rather than risking total default or bankruptcy. However, creditors are never legally required to settle, which is why no debt relief company can guarantee specific results.

How Does Debt Relief Work for Credit Card Debt?

Many people searching how does debt relief work are specifically dealing with high-interest credit card balances.

Credit card debt settlement often involves intentionally allowing accounts to become delinquent so creditors may become more willing to negotiate reduced payoffs.

What Happens During Delinquency?

During delinquency, late fees and interest charges may continue accumulating, and creditors may pursue collection efforts. Some consumers are surprised to learn that collection calls may actually increase during the settlement process.

Credit Score Impact of Debt Settlement

Settled accounts are commonly reported negatively on credit reports. Late payments, charge-offs, and settlement notations can remain on reports for years, affecting future borrowing opportunities.

Are Debt Relief Programs Worth It?

The question are debt relief programs worth it depends entirely on the consumer’s financial condition, goals, and risk tolerance.

For individuals facing severe financial hardship, debt settlement may help reduce overwhelming balances and create a path toward financial recovery.

Situations Where Debt Relief May Help

Debt relief may be considered when consumers are already behind on payments, cannot realistically repay debts in full, or are trying to avoid bankruptcy.

Consumers with high-interest debt and limited disposable income sometimes use settlement programs to regain control of finances.

Situations Where Debt Relief May Cause More Harm

Debt relief may not be ideal for consumers trying to protect strong credit scores or qualify for mortgages, business loans, or other financing in the near future. The long-term credit damage may outweigh short-term settlement savings.

Is Debt Relief a Good Idea for Everyone?

No. Asking is debt relief a good idea requires careful analysis of each consumer’s financial profile.

Factors That Should Be Reviewed First

Before entering a debt relief program, consumers should evaluate income stability, monthly obligations, total debt balances, lawsuit exposure, and long-term financial goals.

Programs advertising “guaranteed debt elimination” or “instant debt freedom” should always be approached cautiously because no company can legally guarantee settlement outcomes before negotiations occur.

Why Personalized Financial Analysis Matters

Debt relief strategies that work for one consumer may create serious problems for another. Some individuals may benefit more from direct creditor negotiations, structured repayment plans, or bankruptcy protections depending on their circumstances.

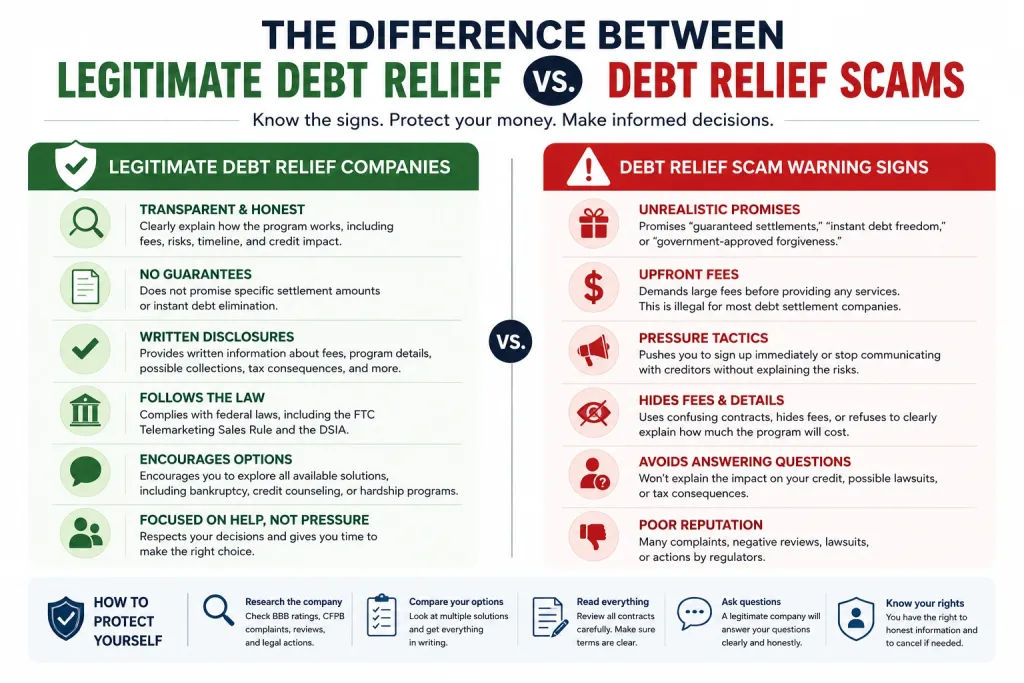

The Difference Between Legitimate Debt Relief and Debt Relief Scams

Consumers asking are debt relief programs legit are often concerned about scams — and for good reason.

Common Warning Signs of Debt Relief Scams

Some companies use aggressive marketing tactics targeting financially distressed individuals. Common warning signs include unrealistic promises, hidden fees, pressure tactics, and misleading claims about credit improvement.

A trustworthy company should clearly explain risks, timelines, fees, and potential consequences before enrollment.

Researching Company Reputation

Consumers researching companies online using searches like total relief services reviews or is debt clear usa legit should carefully review Better Business Bureau records, CFPB complaints, lawsuits, and independent customer feedback.

Is National Debt Relief Worth It?

Many consumers specifically search is national debt relief worth it because large debt settlement companies advertise heavily online and on television.

Questions Consumers Should Ask Before Enrolling

Consumers should review how fees are calculated, how long programs usually last, and what happens if creditors refuse to negotiate or pursue lawsuits.

Understanding the full financial impact is more important than focusing only on monthly payment reductions.

Large Companies Still Require Careful Review

Even large national companies should be evaluated carefully. Advertising size does not automatically guarantee ethical practices or positive outcomes.

Notice of Credit Card Debt Forgiveness and IRS Tax Consequences

One major issue consumers often overlook is the potential tax impact associated with settled debt.

A notice of credit card debt forgiveness usually refers to IRS Form 1099-C, which creditors may issue after forgiving part of a balance.

Why Forgiven Debt May Become Taxable

If a creditor forgives a portion of debt, the IRS may treat the forgiven amount as taxable income. For example, if a consumer settles a $25,000 balance for $10,000, the remaining $15,000 may potentially be taxable.

Insolvency Exceptions and Tax Relief

Some consumers may qualify for insolvency exceptions that reduce or eliminate tax liability associated with forgiven debt. However, these rules are complex and should be reviewed carefully with tax professionals.

Debt Independence Requires More Than Debt Settlement

Many debt relief advertisements promote the idea of financial freedom or debt independence, but long-term recovery requires more than negotiating balances.

Financial Habits Matter

True financial recovery often involves budgeting, emergency savings, responsible borrowing habits, and long-term financial planning.

Without behavioral and financial changes, consumers may eventually return to debt even after settlements are completed.

Credit Rebuilding After Debt Relief

Consumers who complete settlement programs usually need to rebuild credit gradually through consistent payment history, controlled credit utilization, and responsible financial management.

Self Debt Negotiation vs Professional Debt Relief Companies

Some consumers attempt self debt negotiation instead of hiring third-party debt settlement companies.

Advantages of Self-Negotiation

Consumers who negotiate directly with creditors may reduce fees and maintain greater control over settlement discussions. Some creditors also offer hardship programs directly to borrowers.

When Professional Guidance May Become Necessary

Complex financial situations involving lawsuits, tax obligations, or multiple collection agencies may require legal or financial assistance beyond self-negotiation.

Alternatives to Debt Relief Programs

Debt settlement is only one option among several possible financial solutions.

Debt Consolidation and Credit Counseling

Some consumers qualify for debt consolidation loans with lower interest rates, while others benefit from nonprofit credit counseling programs that organize structured repayment plans.

Bankruptcy and Legal Protections

In severe financial hardship situations, bankruptcy may provide stronger legal protections against collection activity, lawsuits, and wage garnishments.

How to Evaluate Whether a Debt Relief Company Is Legitimate

Consumers researching are debt relief programs legit should evaluate companies carefully before providing financial information or signing contracts.

Important Questions to Ask

Consumers should ask about fees, settlement timelines, complaint history, licensing status, and written disclosures before enrolling in any program.

Transparency Is a Major Trust Signal

Legitimate companies should clearly explain credit risks, tax consequences, possible lawsuits, and estimated settlement outcomes without making unrealistic promises.

Final Thoughts — Are Debt Relief Programs Legit?

Yes, some debt relief programs are legitimate and may help consumers reduce financial pressure under certain circumstances. However, not every company offering debt settlement services operates ethically or transparently.

Consumers searching are debt relief programs legit should understand that debt settlement carries real financial consequences including credit score damage, tax exposure, collection activity, and potential legal risks.

Debt relief may help some individuals avoid bankruptcy or regain financial stability, but it should never be approached without understanding the full long-term impact.

The safest approach is to compare all available options, review contracts carefully, research companies thoroughly, and seek professional legal or tax guidance when necessary.

Frequently Asked Questions

Are debt relief programs legit or scams?

Some debt relief programs are legitimate, while others use misleading marketing tactics. Consumers should research reviews, complaints, and regulatory history carefully before enrolling.

How badly does debt relief affect credit scores?

Debt settlement often causes significant credit score damage because accounts usually become delinquent during negotiations.

Are debt relief programs worth it for credit card debt?

They may help consumers facing serious hardship, but the risks, fees, tax consequences, and credit damage should always be evaluated first.

What happens after debt forgiveness?

Creditors may issue a 1099-C form reporting forgiven debt as potential taxable income to the IRS.

Is debt relief better than bankruptcy?

It depends on the individual financial situation. Bankruptcy may provide stronger legal protections in severe hardship cases.

Can I negotiate debt myself?

Yes. Some consumers successfully negotiate directly with creditors without using third-party settlement companies.

This article is for educational purposes only and does not constitute legal or tax advice. Viewing this page does not create an attorney-client relationship. IRS outcomes depend on your specific financial situation, documentation, compliance status, and procedural posture. If you have received time-sensitive IRS notices, seek qualified professional advice promptly.