Tax Relief Programs are often misunderstood, heavily marketed, and frequently misrepresented, especially when taxpayers are facing IRS notices, wage garnishments, bank levies, or growing penalties. As of 2026, IRS enforcement activity continues to evolve, with expanded automation, faster levy cycles, and more rigorous financial verification processes. Understanding how official Tax Relief Programs actually work under federal law is no longer optional, it is critical for protecting your income and assets.

Many taxpayers searching for Tax Relief Programs encounter terms like “tax forgiveness,” “hardship program,” or “Fresh Start,” without realizing these are marketing phrases rather than standalone legal programs. In reality, legitimate Tax Relief Programs are governed by specific provisions of the Internal Revenue Code and strict IRS procedural rules. Options such as Offer in Compromise, Installment Agreements, Currently Not Collectible (CNC) status, and Collection Due Process hearings all require full compliance, detailed financial disclosure, and proper strategic positioning.

At Tax Law Advocates, our team brings decades of combined experience representing individuals and small businesses before IRS Revenue Officers, the Automated Collection System (ACS), and the IRS Office of Appeals nationwide. In our experience, taxpayers often attempt to apply for Tax Relief Programs without fully understanding documentation requirements, qualification standards, or enforcement timelines, leading to rejected submissions or accelerated collection actions. We have seen firsthand how early professional evaluation can prevent costly mistakes and improve strategic outcomes. This guide explains Tax Relief Programs clearly, accurately, and transparently, so you can understand your rights and options before the IRS escalates enforcement.

What’s Changed Recently in Tax Relief Programs: Updated for 2026

As of 2026, taxpayers navigating IRS collection activity are facing a more technologically advanced and compliance-driven enforcement environment. While core Tax Relief Programs such as Offer in Compromise, Installment Agreements, and Currently Not Collectible (CNC) status remain available, the IRS has tightened procedures, enhanced digital monitoring, and increased documentation scrutiny. Understanding these updates is essential before applying for any of the major Tax Relief Programs.

Below are the most significant enforcement and procedural shifts affecting taxpayers in 2026.

Expanded Digital Enforcement and Automated Levy Cycles

The IRS continues expanding automation within its Automated Collection System (ACS). As of 2026, levy cycles move faster once a Final Notice of Intent to Levy (LT11 or Letter 1058) expires. Automated bank levies and wage garnishments are often triggered more quickly when taxpayers fail to respond within the 30-day appeal window.

This means taxpayers exploring Tax Relief Programs must act earlier in the notice timeline. Waiting until after a levy hits a bank account significantly limits strategic flexibility. In our experience representing taxpayers before ACS and Revenue Officers, proactive filings — such as timely Collection Due Process (CDP) requests, are increasingly important to preserve rights and suspend enforcement.

Increased Scrutiny in Offer in Compromise (OIC) Reviews

Offer in Compromise submissions are receiving deeper financial verification in 2026. The IRS is cross-checking:

- Bank deposits against reported income

- Digital payment platforms

- Business gross receipts

- Cryptocurrency disclosures

While Offer in Compromise remains one of the most powerful Tax Relief Programs, approval depends heavily on accurate Reasonable Collection Potential (RCP) calculations. Incomplete documentation, inconsistent income reporting, or overstated expenses are more likely to result in returned or rejected applications.

In our experience, properly structured OIC submissions, supported by detailed financial analysis, significantly reduce unnecessary delays and procedural returns.

Inflation-Adjusted Allowable Living Expense Standards

Each year, the IRS updates National and Local Standards for allowable living expenses. In 2026, these standards reflect inflation adjustments in housing, transportation, and food categories.

These changes directly impact calculations for several Tax Relief Programs, including Installment Agreements and CNC determinations. Taxpayers may qualify for lower monthly payment obligations if expenses fall within updated IRS standards. However, exceeding standard allowances still requires documented justification.

Strategic expense categorization remains critical during financial disclosure preparation.

More Frequent CNC Compliance Monitoring

Currently Not Collectible (CNC) status remains available for taxpayers experiencing financial hardship. However, in 2026, the IRS is conducting more frequent compliance reviews. This includes mid-cycle income checks and verification of new employment data.

Although CNC is one of the recognized Tax Relief Programs, it is temporary. Interest continues accruing, and improved financial conditions may result in removal from hardship status. Taxpayers must remain compliant with future filings to maintain protection from enforced collection.

Tighter Business Income Verification for Installment Agreements

For self-employed individuals and business owners, installment agreement approvals now involve deeper review of gross receipts and operational expenses. The IRS increasingly analyzes:

- Profit and loss statements

- Merchant processing reports

- Bank deposit consistency

Business taxpayers pursuing Tax Relief Programs in 2026 should prepare comprehensive financial documentation to avoid delays.

Understanding these 2026 enforcement trends is essential before engaging in any IRS resolution strategy. While Tax Relief Programs remain available, procedural precision, compliance history, and accurate financial disclosure now play a larger role than ever in achieving sustainable outcomes.

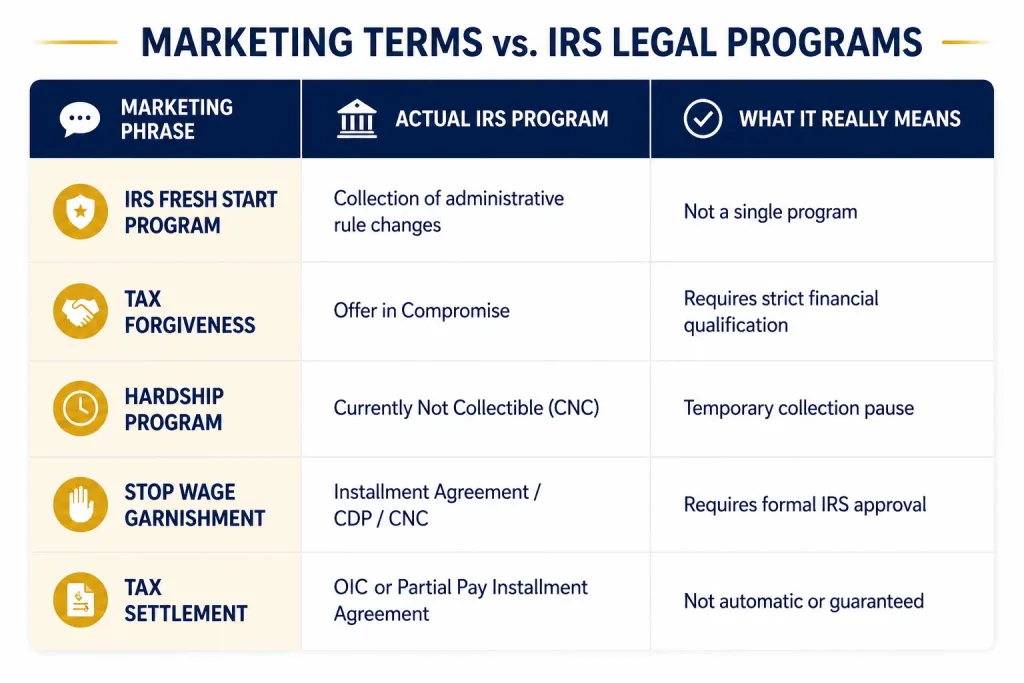

Tax Relief Marketing vs. Actual IRS Programs

One of the biggest problems taxpayers face is confusing marketing language with IRS law.

Important: No private company “approves” forgiveness. Only the IRS administers relief programs under federal law.

Tax Relief Marketing vs. Actual IRS Programs (2026 Reality Check)

One of the biggest problems taxpayers face is confusing marketing language with actual IRS law. When you’re under stress , facing wage garnishment, a bank levy, or threatening IRS letters , phrases like “tax forgiveness,” “fresh start,” or “hardship program” can sound like guaranteed solutions. In reality, many of these terms are marketing labels, not official program names found in the Internal Revenue Code.

As of 2026, the IRS continues warning taxpayers about misleading tax relief advertising. Understanding the difference between Tax Relief Programs that exist under federal law and promotional language used in commercials is essential to protecting yourself financially.

Below is a clear breakdown.

“IRS Fresh Start Program” – What It Really Is

There is no standalone “Fresh Start Program” application. The term refers to a series of IRS policy adjustments introduced years ago that expanded access to existing Tax Relief Programs, including streamlined installment agreements and modified Offer in Compromise guidelines.

Marketing materials often imply Fresh Start is a special forgiveness track. It is not. Taxpayers must still qualify under standard IRS rules and submit full financial disclosures.

“Tax Forgiveness” – A Misleading Shortcut

The phrase “tax forgiveness” is commonly used to describe an Offer in Compromise (OIC). However, an OIC is not an automatic forgiveness. It is a negotiated settlement under IRC §7122, approved only if the IRS determines it cannot reasonably collect the full amount within the statutory period.

Qualification requires:

- Filing all required tax returns

- Submitting Form 433 financial statements

- Disclosing assets, income, and expenses

- Passing a Reasonable Collection Potential (RCP) analysis

In our experience representing taxpayers nationwide, many rejected applications stem from unrealistic expectations shaped by marketing promises rather than IRS standards.

“Hardship Program” – Temporary, Not Permanent

The “hardship program” typically refers to Currently Not Collectible (CNC) status. CNC pauses active collection when paying would prevent you from meeting basic living expenses. It does not eliminate debt. Interest continues accruing, and the IRS reviews financial status periodically.

Taxpayers must remain compliant with filings to stay in CNC status.

“Stop Wage Garnishment” – A Result, Not a Program

No company can simply “stop” a garnishment. Collection activity stops only after the IRS formally accepts:

- An Installment Agreement

- An Offer in Compromise

- A CNC determination

- A timely Collection Due Process (CDP) request

These outcomes are results of engaging official Tax Relief Programs, not standalone services sold by private firms.

“Tax Settlement” – Not Guaranteed

“Tax settlement” usually means an OIC or Partial Pay Installment Agreement. Both require proof of limited ability to pay. Approval depends on documented financial hardship and compliance history. There are no guarantees under federal law.

Important Warning for Taxpayers (2026)

No private company approves forgiveness. Only the IRS administers Tax Relief Programs under federal law. Be cautious of firms that:

- Guarantee “pennies on the dollar”

- Charge high upfront fees before review

- Refuse to explain eligibility criteria

- Claim they can stop IRS action instantly

A legitimate resolution strategy requires legal qualification, documented evidence, and adherence to IRS procedures. Understanding the difference between marketing language and real Tax Relief Programs is the first step toward protecting your financial stability.

IRS Tax Relief Programs Explained (2026): Offer in Compromise (OIC)

Among all available Tax Relief Programs, the Offer in Compromise (OIC) is one of the most powerful , and one of the most misunderstood. An Offer in Compromise allows qualified taxpayers to settle tax debt for less than the full amount owed if the IRS determines it cannot collect the entire balance within a reasonable period of time. However, approval is not automatic, and qualification standards remain strict in 2026.

Under Internal Revenue Code §7122, the IRS may accept an Offer in Compromise on three legal grounds:

- Doubt as to Collectibility – You cannot realistically pay the full debt through assets or income.

- Doubt as to Liability – There is legitimate dispute regarding whether the tax was assessed correctly.

- Effective Tax Administration – The debt is legally owed and collectible, but requiring full payment would create economic hardship or be unfair based on special circumstances.

While many marketing materials describe OIC as “tax forgiveness,” it is important to understand that this is one of several structured Tax Relief Programs governed by federal law. The IRS evaluates OIC applications using detailed financial analysis, not promotional claims.

How the IRS Calculates Your Offer (RCP Formula)

The IRS determines whether to accept an offer by calculating your Reasonable Collection Potential (RCP). This formula represents the total amount the IRS believes it can collect from you before the 10-year collection statute expires.

RCP generally includes:

- Net Realizable Equity in Assets

This includes real estate, vehicles, retirement accounts, business interests, and other property. The IRS calculates quick-sale value (usually 80% of fair market value) minus encumbrances. - Monthly Disposable Income × 12 or 24 Months

The multiplier depends on the payment option selected:- Lump sum offer: 12 months of future disposable income

- Periodic payment offer: 24 months of future disposable income

- Lump sum offer: 12 months of future disposable income

- Disposable income is calculated after subtracting allowable living expenses based on IRS National and Local Standards.

- Future Earning Potential

The IRS evaluates consistency of income, employment history, and likelihood of continued earnings.

If your calculated RCP equals or exceeds the total tax debt, the IRS will generally reject the offer. That is why proper financial preparation is critical when pursuing this option within the broader framework of Tax Relief Programs.

2026 Enforcement and Documentation Trends

As of 2026, the IRS has increased financial verification in OIC reviews. Bank deposits, business gross receipts, and digital income platforms are cross-checked against reported figures. Incomplete Form 433 submissions frequently result in returned applications rather than formal denials.

In our experience representing taxpayers before Revenue Officers and the IRS Offer Unit, one of the most common mistakes is submitting an offer without fully analyzing RCP first. Many taxpayers assume that simply having hardship qualifies them for settlement. In reality, the IRS focuses on mathematical collectibility.

Important Considerations Before Applying

Before pursuing this option under federal Tax Relief Programs, taxpayers must:

- File all required tax returns

- Make required estimated payments (if self-employed)

- Remain compliant during review

- Submit full financial disclosure

An Offer in Compromise can be an effective resolution tool when properly structured. However, it is not guaranteed, and eligibility depends entirely on financial facts and compliance status. Understanding how the IRS evaluates offers under Tax Relief Programs is essential before submitting an application in 2026.

Take Action Before the IRS Escalates

When it comes to IRS debt, timing is everything. Many taxpayers wait until a wage garnishment begins or a bank account is levied before exploring their options. By that stage, your negotiating flexibility may already be limited. Acting early , before enforcement escalates , gives you access to the full range of Tax Relief Programs and preserves important procedural rights.

The IRS follows a structured collection timeline. It begins with balance due notices (such as CP14), progresses to more urgent warnings (CP504), and ultimately leads to a Final Notice of Intent to Levy (LT11 or Letter 1058). Once that final notice is issued, you typically have only 30 days to request a Collection Due Process hearing. Missing that deadline can allow the IRS to garnish wages, levy bank accounts, or seize assets.

Engaging available Tax Relief Programs before enforcement begins can often prevent aggressive collection actions. Options such as Installment Agreements, Offer in Compromise, or Currently Not Collectible status require formal IRS approval, but when initiated early, they may suspend collection activity and reduce financial disruption.

As of 2026, automated enforcement systems move faster than in prior years. The IRS uses digital tools to verify income and trigger levy cycles more efficiently. Waiting for the situation to “work itself out” rarely produces favorable results. Strategic use of legitimate Tax Relief Programs must be timely, compliant, and properly documented.

If you have received escalating IRS notices or fear a levy may be imminent, now is the time to evaluate your eligibility under federal Tax Relief Programs. Early action can protect income, preserve appeal rights, and create a structured path toward resolution before the IRS escalates further.

Why Experience Matters in IRS Cases (2026 Perspective)

IRS collection cases are not simply paperwork exercises , they are procedural negotiations governed by federal law, internal revenue manuals, and strict deadlines. In our experience representing taxpayers nationwide before Revenue Officers, the Automated Collection System (ACS), and the IRS Office of Appeals, outcomes often hinge on technical accuracy and timing rather than emotion or urgency.

Revenue Officers expect detailed substantiation. When financial statements are submitted, they are reviewed line by line. Bank deposits are compared against reported income. Asset valuations are analyzed for equity discrepancies. If supporting documentation is incomplete or inconsistent, credibility is immediately weakened.

Financial misstatements , even unintentional ones , frequently trigger rejections, returned submissions, or additional scrutiny. For example, overstating allowable expenses or undervaluing assets in an Offer in Compromise (OIC) filing can delay resolution for months. In more serious cases, discrepancies may prompt further investigation.

Poorly structured OIC submissions lose leverage. An Offer in Compromise must be calculated according to the IRS Reasonable Collection Potential (RCP) formula. Submitting an offer without first analyzing RCP often results in rejection because the IRS determines the taxpayer has the ability to pay more. Once rejected, negotiating flexibility may decrease.

Missing deadlines can result in immediate levy action. If a Final Notice of Intent to Levy (LT11 or Letter 1058) expires without a timely Collection Due Process (CDP) request, the IRS can garnish wages or levy bank accounts. Appeals rights are procedural and time-sensitive. Understanding enforcement timing is critical.

IRS representation requires working knowledge of procedural law, Appeals processes, statute of limitations rules, and collection alternatives. Experience matters because IRS systems are structured, technical, and deadline-driven.

Taxpayer Rights (Taxpayer Bill of Rights)

Even during enforcement, taxpayers are protected by the Taxpayer Bill of Rights. Every taxpayer has:

- The Right to Be Informed – Clear explanations of IRS decisions and notices.

- The Right to Appeal – Access to an independent review by the IRS Office of Appeals.

- The Right to Finality – Knowledge of deadlines and time limits for collection.

- The Right to Retain Representation – The ability to hire an attorney, CPA, or Enrolled Agent.

These rights are not theoretical. They are enforceable protections embedded in federal tax administration. Exercising them properly requires understanding how and when to invoke procedural safeguards.

Common Taxpayer Mistakes in 2026

As of 2026, several recurring mistakes continue to jeopardize IRS cases:

- Ignoring Early Notices

Many taxpayers delay action until a levy is imminent, reducing available options. - Submitting Incomplete Financial Forms

Missing attachments or unsupported expense claims often result in returned applications. - Believing Marketing Guarantees

Promises of “pennies on the dollar” without financial review create unrealistic expectations. - Failing to File Required Returns

The IRS will not approve most resolution options unless all filings are current. - Missing Appeal Deadlines

A missed 30-day CDP window can eliminate important procedural protections.

Underestimating Business Income Review

Self-employed individuals face increased scrutiny of bank deposits and gross receipts.

IRS matters are rarely resolved by chance. They are resolved through compliance, documentation, and procedural awareness. Understanding your rights — and avoiding common mistakes , can significantly impact the direction and outcome of your case.

Frequently Asked Questions

Is the IRS Fresh Start Program real?

It refers to administrative updates, not a standalone program.

Can I settle for pennies on the dollar?

Only if your financial disclosure proves inability to pay.

Does filing an OIC stop garnishment?

Generally, collection pauses while pending, but timing matters.

Does CNC erase debt?

No, it pauses the collection temporarily.

How long does the IRS have to collect?

Generally 10 years from assessment, subject to tolling

Conclusion: Protect Your Financial Future Before the IRS Decides for You

IRS tax debt does not disappear on its own. Interest continues to accrue. Penalties compound. Enforcement timelines move forward whether you are prepared or not. As of 2026, with expanded automation and tighter financial verification, waiting often limits your options rather than improves them.

Understanding IRS procedures, qualifying correctly for relief, and responding within strict deadlines can make the difference between structured resolution and aggressive collection. Whether you are considering an Offer in Compromise, Installment Agreement, Currently Not Collectible status, or defending against a levy, the strategy must align with federal law and your documented financial reality.

In our experience representing taxpayers nationwide, early intervention consistently provides more leverage. Properly structured submissions, accurate financial disclosure, and timely appeals can prevent wage garnishments, bank levies, and escalating enforcement. Conversely, incomplete filings, missed deadlines, or reliance on unrealistic marketing promises can significantly delay or damage your case.

Tax Law Advocates bring decades of combined experience in IRS representation, working directly with Revenue Officers, the Automated Collection System, and the IRS Office of Appeals. We approach every case with legal precision, transparency, and strategic evaluation , not guarantees or shortcuts. Every taxpayer’s financial situation is unique, and every resolution strategy must be built on verified facts and procedural compliance.

If you are facing IRS notices, mounting penalties, or the risk of enforced collection, now is the time to act. A confidential case evaluation can clarify your options, assess eligibility, and outline a realistic path forward.

Contact Tax Law Advocates today to review your situation before the IRS escalates further. The right strategy , applied at the right time , can protect your income, assets, and long-term financial stability.