Understanding the Tax Implications of Divorce Before the IRS Gets Involved

The Tax Implications of Divorce can affect your financial future long after a judge signs the final decree. As tax attorneys at Tax Law Advocates, we frequently represent individuals who believed their divorce agreement resolved every financial obligation, only to discover that the IRS follows federal tax law—not family court orders. In many cases, joint tax liability survives divorce, and the IRS can pursue either spouse for unpaid taxes regardless of what the divorce settlement says. Understanding the Tax Implications of Divorce before finalizing a settlement can help you avoid wage garnishments, bank levies, federal tax liens, and costly IRS disputes.

Divorce affects far more than your filing status. It can determine who remains responsible for prior tax debts, who qualifies for valuable child-related tax credits, how alimony is treated under current federal law, and how the IRS views business income, deductions, penalties, and interest. In 2026, the IRS continues to aggressively enforce collection actions involving unpaid joint tax balances and underreported income, especially when one spouse controlled the household finances during the marriage. Without a strategic review of the Tax Implications of Divorce, one spouse may face significant financial exposure years after the divorce becomes final.

From our experience representing taxpayers before IRS Revenue Officers and the IRS Independent Office of Appeals, we have seen many post-divorce tax disputes that proper planning could have prevented. Whether you need to allocate responsibility for back taxes, pursue Innocent Spouse Relief, resolve existing tax liens, or negotiate payment arrangements before dividing assets, timing matters. The Tax Implications of Divorce involve much more than tax compliance—they require proactive legal and financial risk management. By addressing these issues early and working with experienced tax counsel, you can protect your rights, reduce future exposure, and move forward with greater financial certainty.

Tax Implications of Divorce Updated for 2026: What’s Changed Recently?

As of 2026, understanding the Tax Implications of Divorce requires more than reviewing filing status and dividing deductions. Recent IRS procedural updates and enforcement trends have increased the complexity and risk associated with divorce-related tax planning. If you separate or finalize a divorce without evaluating the Tax Implications of Divorce under current rules, you may face IRS enforcement actions years after the court finalizes your decree.

Inflation Adjustments and Credit Phaseouts

For 2026, the IRS increased federal tax brackets, the standard deduction, and several tax credits to account for inflation. Although these adjustments may seem routine, they can significantly affect divorcing taxpayers, especially those who rely on child-related credits and income-based tax benefits. The IRS applies income thresholds to the Child Tax Credit and other dependent-related benefits, and post-divorce changes in income—such as alimony, business distributions, or asset sales—can affect eligibility. As a result, the Tax Implications of Divorce require careful income forecasting rather than a simple review of prior-year tax returns.

Expanded Automated Enforcement

The IRS continues to expand its automated collection programs. The agency now uses earlier levy triggers, automated balance-due notices, and faster lien filing procedures, allowing collection actions to begin sooner than in previous years. If joint tax debt remains unresolved, the IRS may garnish wages or levy bank accounts even after a divorce becomes final. For that reason, taxpayers should address outstanding tax liabilities before completing the divorce process. When evaluating the Tax Implications of Divorce, proactive tax planning often prevents costly collection actions later.

Enhanced Income Cross-Matching

The IRS has intensified cross-matching of third-party income reporting. Expansion of Form 1099-K reporting thresholds and digital asset (cryptocurrency) disclosure requirements have increased audit exposure. In divorce cases where one spouse operated a business or controlled digital assets, unreported income discovered through IRS data analytics may trigger audits or adjustments to previously filed joint returns. When reassessing the Tax Implications of Divorce, it is essential to review prior filings carefully for accuracy and completeness.

Focus on High-Balance Joint Liabilities

Revenue Officers are prioritizing high-balance joint accounts, especially where collection potential exists. Even if a divorce decree assigns tax responsibility to one spouse, the IRS retains full collection authority against either party under joint and several liability rules. This remains one of the most misunderstood Tax Implications of Divorce. Court orders do not override federal tax law.

Increased Scrutiny of Innocent Spouse Claims

Innocent Spouse Relief applications are receiving greater scrutiny, particularly in cases involving hidden business income, offshore accounts, or cryptocurrency holdings. The IRS now evaluates digital financial footprints more aggressively. Documentation standards remain strict, and incomplete or poorly supported claims face higher denial rates. Individuals considering relief must understand how the evolving enforcement climate affects the Tax Implications of Divorce in 2026.

The Unchanged but Critical Rule

Perhaps most important: as of 2026, the IRS still does not recognize divorce decrees when determining collection rights. That principle remains unchanged , and dangerous if misunderstood. While family courts divide marital responsibility, federal tax law preserves the government’s ability to collect from either spouse on a joint return. Recognizing this core element of the Tax Implications of Divorce can prevent severe financial consequences and allow strategic planning before enforcement escalates.

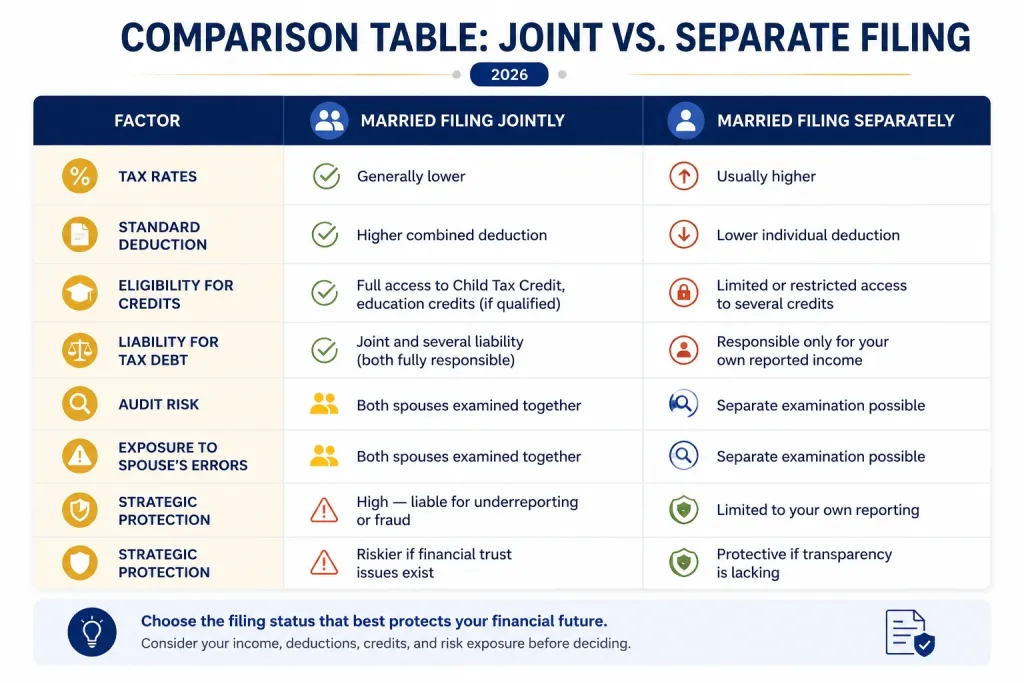

Joint vs. Separate Filing During Separation, long-term Tax Implications of Divorce

One of the most critical decisions couples face during separation is whether to file jointly or separately. This choice has immediate and long-term Tax Implications of Divorce, particularly when trust, income transparency, or prior tax debt is involved. Because your marital status on December 31 determines your filing eligibility for the entire tax year, timing matters. Evaluating the Tax Implications of Divorce at this stage can prevent joint liability exposure that continues long after the relationship ends.

If you are still legally married as of December 31, you may file Married Filing Jointly. Alternatively, you can choose Married Filing Separately. Each option carries distinct risks and benefits.

Filing jointly may reduce your overall tax bill, but it also means accepting full responsibility for the accuracy of the return. Under Internal Revenue Code §6013, both spouses are fully liable for tax, penalties, and interest. Even if one spouse earned most of the income or made reporting errors, the IRS can pursue either party. This remains one of the most misunderstood Tax Implications of Divorce.

Filing separately limits exposure to your own income and deductions, offering protective value during contentious separations. However, it may result in higher tax rates and restricted access to certain credits. The financial trade-off must be weighed carefully against the legal and enforcement risks involved.

In our experience representing taxpayers before Revenue Officers, many post-divorce collection disputes originate from joint returns filed during separation without proper evaluation. The Tax Implications of Divorce extend beyond immediate savings, they involve risk management, compliance protection, and future audit exposure.

Ultimately, choosing the correct filing status requires coordinated planning with both legal and tax professionals. Understanding the Tax Implications of Divorce before submitting your return can mean the difference between temporary savings and long-term liability.

How Existing Tax Debts and IRS Liens Are Allocated

One of the most serious and misunderstood Tax Implications of Divorce involves how existing tax debt and federal tax liens are treated after separation. Many individuals assume that once a divorce decree assigns responsibility for back taxes to one spouse, the matter is settled. Unfortunately, federal tax law operates independently of family court orders. The IRS applies its own rules , and those rules can expose either spouse to full collection action.

Joint Tax Debt

If prior joint tax returns show unpaid balances, both spouses remain fully responsible under the doctrine of joint and several liability. This means:

- Both spouses remain 100% liable for the entire balance

- The IRS may collect from either spouse

- Collection does not split 50/50 automatically

Even if one spouse earned most of the income, operated the family business, or handled all financial reporting, both names on a joint return create full exposure. The IRS is not required to divide responsibility proportionally, nor is it obligated to pursue one spouse before the other.

In practice, the IRS often collects from the spouse who appears more collectible — meaning the one with stable wages, accessible bank accounts, or valuable assets. We have seen situations where a lower-earning spouse becomes the primary target simply because they are easier to collect from. This is one of the most financially dangerous Tax Implications of Divorce, particularly when joint returns involve complex income sources, business deductions, or unreported earnings.

Additionally, penalties and interest continue accruing until the balance is resolved. A delayed response can significantly increase the total amount owed.

IRS Liens

When tax debt remains unpaid, the IRS may file a Notice of Federal Tax Lien. A federal tax lien attaches broadly to:

- Real estate

- Bank accounts

- Business interests

- Future property interests

The scope of a lien is often underestimated. It not only attaches to property currently owned but can also attach to property acquired in the future while the debt remains outstanding.

If a lien is filed before divorce, it can create substantial complications during property division. For example:

- A home sale may be delayed because the lien must be satisfied or negotiated before clear title can transfer.

- Asset transfers between spouses may be restricted.

- Refinancing efforts may be blocked by the lien’s presence.

In some cases, divorcing spouses agree that one party will keep the home, only to discover that the IRS lien prevents refinancing unless the tax debt is addressed. These complications underscore the importance of evaluating the Tax Implications of Divorce before finalizing asset distribution.

Because divorce courts cannot extinguish federal tax liens, resolving or restructuring the debt proactively is often essential. Options may include installment agreements, lien subordination, partial releases, or other negotiated resolutions, each dependent on compliance and financial disclosure.

Understanding how joint tax debts and liens operate is critical to protecting your financial future. Divorce may divide assets between spouses, but without strategic tax planning, the IRS retains powerful collection rights that survive the marriage.

Innocent Spouse Relief (2026 Guide)

One of the most important protections available under the Tax Implications of Divorce framework is Innocent Spouse Relief. When a joint tax return contains errors, underreported income, improper deductions, or hidden assets, both spouses are normally held fully responsible. However, federal law recognizes that in some marriages, one spouse may not have known , and had no reason to know about the financial misconduct of the other.

Innocent Spouse Relief, governed by Internal Revenue Code §6015, allows qualifying individuals to request removal or reduction of joint tax liability. As of 2026, the IRS continues to review these applications carefully, particularly in cases involving business income, digital assets, or complex financial structures. The Tax Implications of Divorce often become most severe when one spouse controlled the finances and the other signed returns without full understanding.

There are three primary forms of relief:

- Innocent Spouse Relief – Available when tax was understated due to the other spouse’s error and the requesting spouse did not know, or have reason to know, of the issue at the time of signing.

- Separation of Liability Relief – Designed for divorced or legally separated individuals. The IRS allocates tax responsibility between spouses based on each person’s income and deductions.

- Equitable Relief – Applies when strict qualification rules are not met but fairness supports relief, such as cases involving financial control, abuse, or deception.

Timing is critical. Applications generally must be filed within specific statutory deadlines. The IRS evaluates financial hardship, knowledge of the understatement, and overall fairness when reviewing claims.

Understanding Innocent Spouse Relief is essential when assessing the broader Tax Implications of Divorce, especially where hidden income, business discrepancies, or inaccurate reporting occurred. Proper documentation, detailed timelines, and clear explanations significantly improve the strength of a claim.

Alimony, Child Credits & Property Transfers (2026 Guide)

Divorce reshapes not only family dynamics but also long-term tax planning. Understanding how alimony, child-related credits, and property transfers are treated under current federal law is essential to avoiding unexpected liabilities. These elements often appear straightforward in divorce agreements, yet their tax treatment can create significant financial consequences if misunderstood.

Alimony Rules

Alimony taxation depends entirely on the date the divorce was finalized.

For divorces finalized before January 1, 2019, alimony payments are:

- Deductible for the payer

- Taxable income for the recipient

For divorces finalized after December 31, 2018, under the Tax Cuts and Jobs Act:

- Alimony is not deductible for the payer

- Alimony is not taxable income for the recipient

This shift dramatically changed post-divorce financial planning. Many individuals mistakenly rely on outdated rules when negotiating support agreements. For post-2018 divorces, the tax burden remains entirely with the payer, as there is no offsetting deduction. Proper structuring during settlement discussions is critical to ensure affordability and compliance.

Child Tax Credit (2026 Inflation Adjusted)

Only one parent may claim a child as a dependent each year. In most cases, the custodial parent, defined as the parent with whom the child resides for the majority of the year — claims the Child Tax Credit.

However, divorce agreements may allocate this right differently through Form 8332, allowing the noncustodial parent to claim the credit. For 2026, inflation adjustments slightly modify income phaseouts and thresholds, making income forecasting important when determining eligibility.

Improper or duplicate claims often trigger IRS notices, audits, and refund delays. Clear documentation and consistent filing are essential.

Property Transfers Under IRC §1041

Internal Revenue Code §1041 governs property transfers incident to divorce. Generally, transfers between spouses or former spouses as part of a divorce settlement are non-taxable events at the time of transfer.

However, this does not eliminate future tax consequences.

The receiving spouse assumes the original cost basis of the asset. When the property is later sold, capital gains taxes are calculated based on that original basis. For example, if one spouse receives the marital home with significant appreciation, future sale proceeds may generate substantial taxable gain depending on exclusion eligibility and holding period.

Strategic evaluation of basis, appreciation potential, and timing of sale is essential during asset division negotiations.

Common Taxpayer Mistakes During Divorce

Even well-intentioned individuals frequently make costly errors during separation. The most common include:

- Assuming a divorce decree binds the IRS. Federal tax law controls IRS collection rights, not family court orders.

- Ignoring unfiled returns. Unfiled years can trigger substitute returns and inflated tax assessments.

- Failing to check for IRS liens. Liens can block property transfers and refinancing.

- Delaying Innocent Spouse Relief applications. Statutory deadlines apply.

- Selling property without resolving liens. This can delay closing or redirect sale proceeds to the IRS.

- Failing to update Form W-4 withholding. Incorrect withholding can lead to underpayment penalties in the first post-divorce year.

Divorce is already financially complex. Careful coordination between legal and tax professionals ensures that support payments, credits, and asset transfers are structured in a way that protects long-term stability and prevents avoidable IRS disputes.

Real-World Case Example (Hypothetical)

A client came to us two years after finalizing her divorce, shocked to discover that the IRS had begun garnishing her wages. During the divorce proceedings, the settlement agreement clearly stated that her former spouse would be responsible for approximately $140,000 in joint tax debt. She believed the issue had been resolved and trusted that he would handle the obligation as ordered by the court.

Unfortunately, he defaulted.

Because the couple had filed joint tax returns, the IRS retained full collection authority against both parties under joint and several liability rules. The agency was not bound by the divorce decree. Once the account became seriously delinquent, automated enforcement progressed. A Final Notice of Intent to Levy had been issued, and when no payment arrangement was secured, the IRS moved forward with wage garnishment.

By the time she contacted our office, significant financial pressure had already begun. Immediate action was necessary.

First, we filed a request for Innocent Spouse Relief, presenting documentation that she had limited knowledge of the business income discrepancies that created much of the liability. At the same time, we opened direct negotiations with the assigned Revenue Officer to prevent further enforcement while her relief request was under review.

To stabilize the situation, we negotiated a Partial Payment Installment Agreement based on her current financial ability. This structured arrangement demonstrated good-faith compliance and secured a levy release, restoring her full paycheck and stopping immediate collection pressure.

Without intervention, enforcement would have escalated. Bank levies, asset seizures, and continued wage garnishment were realistic next steps. This case illustrates a critical reality: divorce settlements do not shield you from federal tax collection. Proactive representation can mean the difference between financial recovery and prolonged IRS enforcement.

Why Experience Matters in IRS Divorce Cases

Family Court Orders Do Not Control IRS Collection Rights

Divorce courts divide marital assets and liabilities, but they do not control how the IRS enforces federal tax law. Even when a divorce decree assigns tax responsibility to one spouse, the IRS may still pursue either spouse for the full amount of a joint tax debt. Understanding this distinction is critical when evaluating post-divorce tax exposure.

Divorce Attorneys and Tax Resolution Attorneys Serve Different Roles

Family law attorneys excel at handling custody disputes, support obligations, and property division. However, most do not regularly manage IRS appeals, Offer in Compromise negotiations, penalty abatement requests, or Revenue Officer enforcement actions. Divorce-related tax liabilities often require a separate strategy focused on federal tax law and IRS procedures.

Revenue Officer Cases Require Immediate Strategic Action

Once the IRS assigns a Revenue Officer to a case, collection activity can escalate quickly. Revenue Officers can issue levies, file federal tax liens, request detailed financial disclosures, and pursue asset seizures. Effective representation requires accurate financial documentation, strategic negotiations, and a thorough understanding of IRS collection procedures.

Technical IRS Programs Demand Specialized Knowledge

Many taxpayers assume that financial hardship alone qualifies them for relief. In reality, programs such as Offer in Compromise, Innocent Spouse Relief, and penalty abatement involve strict legal and financial standards. Successful applications require detailed calculations, supporting documentation, and a clear understanding of IRS evaluation criteria.

Missing IRS Deadlines Can Eliminate Important Rights

IRS enforcement procedures often involve strict deadlines. For example, failing to request a Collection Due Process hearing within the required timeframe can limit appeal rights and accelerate collection actions. Taxpayers frequently discover these deadlines only after enforcement has already begun.

Coordinating Divorce Strategy With Tax Resolution Planning

The most effective approach addresses divorce and tax issues simultaneously. Evaluating tax liabilities before dividing assets, transferring property, or finalizing support obligations can prevent future disputes and reduce exposure to IRS enforcement. Early planning often creates more resolution options and better financial outcomes.

Protecting Your Financial Future After Divorce

Divorce may end a marriage, but it does not automatically end federal tax liability. Strategic tax representation helps align divorce settlements with federal tax obligations, reducing risk and protecting long-term financial stability. The sooner taxpayers address potential IRS issues, the more options they typically have available.

Frequently Asked Questions

Does divorce remove my responsibility for joint tax debt?

No. The IRS can collect from either spouse regardless of divorce decree terms.

Can I qualify for Innocent Spouse Relief after divorce?

Yes, if eligibility criteria under IRC §6015 are met.

Who claims the child tax credit after divorce?

Typically the custodial parent unless otherwise specified.

Can the IRS levy me for my ex’s tax fraud?

Yes, unless relief is approved.

Does filing separately protect me from old tax debt?

No, only future liabilities.

Conclusion: Protect Your Financial Future Before the IRS Decides for You

Divorce is already one of life’s most emotionally and financially draining transitions. When federal tax liabilities are added to the equation, the consequences can extend far beyond the courtroom. As we’ve outlined, joint tax debt does not disappear when a marriage ends. IRS liens can attach to property even after assets are divided. Child credits must be carefully allocated. Alimony rules have changed. And Innocent Spouse Relief requires precise documentation and strategic timing.

Perhaps most importantly, the IRS is not bound by your divorce decree.

Under joint and several liability rules, either spouse can be pursued for the full balance of unpaid tax. That means wage garnishments, bank levies, and property liens can surface years after a divorce is finalized, often when one party least expects it. In 2026, with expanded automated enforcement and heightened scrutiny of financial disclosures, the margin for error is smaller than ever.

The key takeaway is simple: divorce settlements must be coordinated with federal tax strategy. Filing status decisions, debt negotiations, lien resolution, and relief applications should be handled proactively, not reactively after enforcement begins. When tax and legal strategy are aligned early, financial risk is significantly reduced.

At Tax Law Advocates, we represent individuals nationwide facing complex IRS issues tied to divorce and separation. Our licensed tax attorneys understand both the procedural realities of IRS collection and the emotional weight of marital dissolution. We negotiate directly with Revenue Officers, prepare structured relief applications, resolve liens before property transfers, and design long-term compliance strategies that allow you to move forward with clarity.

If you are currently going through a divorce, or if you finalized one and now face IRS notices, joint tax debt, or wage garnishment, do not wait for enforcement to escalate. Early intervention creates more options and better outcomes.

Your financial independence deserves protection.

Call 855-612-7777 today to schedule your confidential case review, or request a consultation online to see if you qualify for relief.

Tax Law Advocates , experienced representation when your future is on the line.

Important Legal Disclaimer (Updated 2026)

This article provides general informational guidance and does not constitute legal advice. Eligibility for IRS programs depends on individual financial circumstances and compliance status. Results are not guaranteed. Always consult a licensed tax professional before making financial decisions.