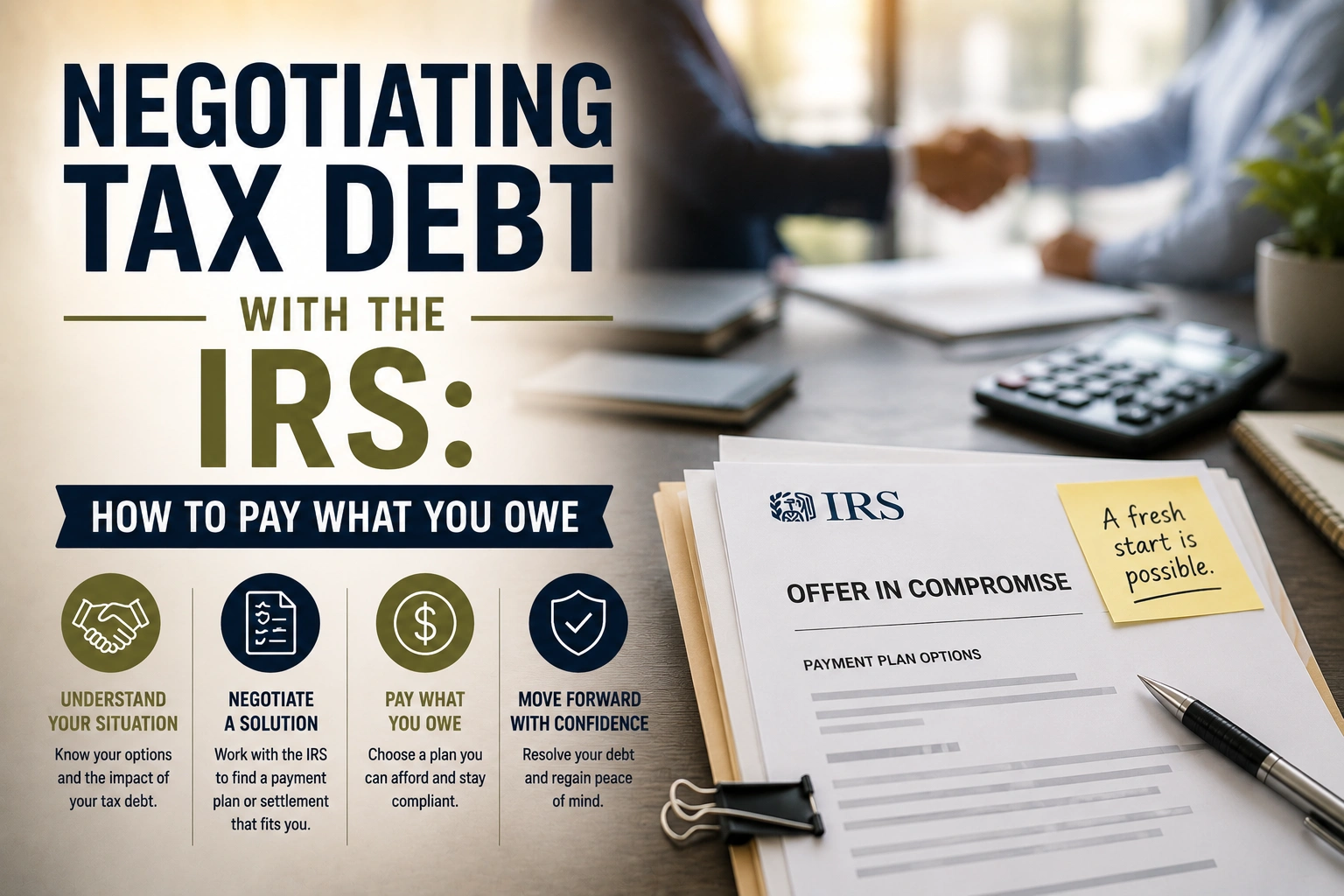

Owing the IRS can be overwhelming, especially when interest and penalties keep adding up. But the good news is the IRS has several programs to help taxpayers negotiate their debt and find a solution.

Whether you owe a few thousand or tens of thousands, there are legal ways to reduce your balance, set up a payment plan or even settle for less than you owe. In this guide we’ll walk you through the main IRS negotiation options and how to choose the one that’s right for you.

If you have unpaid taxes, Tax Law Advocates can help you navigate the negotiation process, protect your assets and get the best possible outcome.

Why Negotiating Tax Debt Matters

Ignoring tax debt only makes it worse. The IRS has broad powers to collect what you owe, including levies, wage garnishments and tax liens. But once you open up and show good faith, the agency will often work with you.

Negotiation allows you to:

- Stop or avoid IRS collection actions

- Reduce penalties and interest

- Protect your income and property

- Get back to financial stability while staying compliant

The key is knowing which programs you qualify for and presenting your case correctly.

How to Negotiate Tax Debt with the IRS

The IRS has several options depending on your situation, income and ability to pay.

1. Offer in Compromise (OIC)

An Offer in Compromise allows you to settle your tax debt for less than the full amount owed. It’s for taxpayers who can’t pay in full and whose situation makes full collection unlikely.

The IRS will review your:

- Income and expenses

- Assets and equity

- Future earning potential

If your offer is the most the IRS can reasonably expect to collect, they may accept it.

You can submit an Offer in Compromise using Form 656 and Form 433-A (OIC) for individuals or Form 433-B (OIC) for businesses.

Tip: Offers are not guaranteed, strong financials and reasoning are key. A tax attorney can help prepare your case.There are several types:

- Guaranteed Installment Agreement: For individuals who owe $10,000 or less and meet certain criteria.

- Streamlined Agreement: For balances under $50,000, no extensive financial disclosure required.

- Partial Payment Installment Agreement: For those who can only pay a portion of their balance before the collection period expires.

You can request a plan using Form 9465 (Installment Agreement Request) or apply online through the IRS payment portal.

This stops most collection activity as long as you stay current with your payments and future filings.

2. Currently Not Collectible (CNC) Status

If you can’t pay anything due to financial hardship you may be eligible for Currently Not Collectible status.

This temporarily halts IRS collection activity, including levies and garnishments, while your financial situation stabilizes.

While in CNC status, penalties and interest continue to accrue but the IRS won’t actively pursue payment. You’ll need to provide detailed financial statements (via Form 433-A or 433-F) to prove hardship.

3. Penalty Abatement

If your tax debt grew due to penalties for late filing or payment you may be eligible for Penalty Abatement.

The IRS may reduce or remove penalties if you can show reasonable cause, such as:

- Serious illness or family emergency

- Natural disaster

- Reliance on incorrect professional advice

- First-time penalty (clean compliance history)

Interest on penalties may also be reduced once they’re removed. This can significantly decrease your total balance.

4. Innocent Spouse Relief

If your tax debt is from a joint tax return where your spouse or ex-spouse made errors, underreported income or claimed improper deductions, you may be eligible for Innocent Spouse Relief.

Filing Form 8857 requests separation of liability, so you’re not held responsible for your partner’s mistakes or misconduct.

How the IRS Looks at Your Case

When negotiating with the IRS they look at your ability to pay, not just how much you owe. They review your:

- Monthly income and necessary living expenses

- Value of assets (homes, vehicles, savings)

- Age, health and employment status

- Filing and payment history

The goal is to determine what’s reasonable and fair based on your financial situation.Being open and proactive helps with any relief option.

Common Mistakes When Trying to Negotiate Tax Debt

Many taxpayers unintentionally make the process harder by:

- Ignoring IRS notices or missing deadlines

- Submitting incomplete forms or incorrect information

- Offering too little in an Offer in Compromise

- Trying to handle complex negotiations without professional help

A tax attorney or enrolled agent can help you avoid these pitfalls, so your case is presented correctly and you don’t miss out on critical relief opportunities.

When to Get Professional Help

If you owe more than a few thousand, have unfiled returns or received threatening IRS notices, it’s best to consult a tax relief professional.

At Tax Law Advocates, our attorneys and enrolled agents can:

- Review your financial situation and determine the best negotiation strategy

- Prepare and file the right forms (Form 656, 9465, 433-A/F, etc.)

- Communicate with the IRS on your behalf

- Negotiate fair settlements and protect your rights

How Tax Law Advocates Can Help You Pay Your IRS Debt

Every case is different and the right approach depends on your financial situation, assets and compliance status.

At Tax Law Advocates, we help individuals and businesses:

- Stop IRS collections and wage garnishments

- Negotiate settlements through the Offer in Compromise program

- Set up affordable payment plans or hardship status

- Resolve unfiled returns and get back in compliance

Ready to take control of your IRS debt?

Don’t face the IRS alone. Contact Tax Law Advocates today for a free consultation and let us help you negotiate your tax debt, reduce penalties and protect your finances.